Thank you for the invitation.

Since I was asked to participate in this panel discussion, I have mainly been thinking about one question: what can I actually contribute here?

I do not see myself as one of the great innovators of the accounting profession. I am not a scientist. I am not a software developer. Nor am I the person who invented the next revolutionary audit methodology.

What I am, however, is someone who has spent the past three decades trying to apply available technology within the practical reality of audits, clients, regulations, compliance requirements, and oversight bodies. Sometimes successfully, sometimes less successfully, but always from the conviction that technology only creates value when it is actually used.

I started my career with EY in 1995. In 1999, I qualified as a Chartered Accountant with a thesis titled Auditing on the Digital Highway. Since 2005, I have been building a small boutique audit and data analytics firm together with my colleagues. Twenty-one years later, we are still a relatively small player.

When I look at my fellow panelists, they represent institutions and organizations that are many times larger than Coney Minds.

In a way, that makes it quite special for me to be standing here today.

Because if there is one advantage of operating from a small practice, it is that you get to see innovations collide with the daily realities of clients, accountants, regulators, and employees over many years.

From that perspective, I have not brought answers today. I have brought four questions.

One Slide and five lessons that I have learned during more than thirty years in the profession.

My hope is that these questions will stimulate a broader discussion about innovation in accounting—not merely about technology, but about what innovation has ultimately meant for our profession, our clients, and our societal role.

Question 1 – Are We Actually Using the Technology That Is Available?

My first question may be the simplest one.

Are we actually using the technology that is available?

If the answer is yes, the immediate follow-up question is: to what extent? And if the answer is no, why not?

When I look back at my own career, I see a long series of technologies passing by.

It started early.

In 1996, I was an ACL Champion at EY, at a time when data analytics in auditing was still considered something for enthusiasts rather than a standard part of the audit process.

When we founded Coney Minds in 2005, we became the European reseller and implementation partner of ACL. We eventually sold those activities in 2019, but they gave us a unique insight into how technology is actually adopted within accounting firms and by clients.

After that came data visualization around 2012, process mining from 2013 onwards, machine learning, Python, supporting audit tools such as DataSnipper, generative AI, automated script generation using large language models, and now the first experiments with agentic AI.

Looking at that timeline, what strikes me most is that the technology has almost always been available.

The far more interesting question is why some innovations achieve widespread adoption while others do not.

Why some technologies remain niche after twenty years, while others are embraced by almost everyone within a matter of months.

Perhaps, in the end, that tells us more about people than about technology.

Question 2 – How Much Has the Audit Process Really Changed?

This brings me to my second question.

If we look at all technological developments over the past thirty years, how much has the underlying audit process actually changed?

In other words: has our societal relevance increased or decreased?

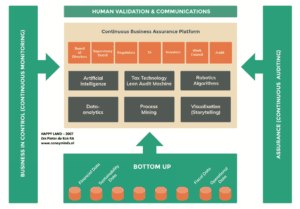

Since around 2007, I have been working on connecting ongoing monitoring within organizations with ongoing auditing by external auditors.

It was—and perhaps still is—my professional dream to bring those two worlds closer together.

To be honest, reality has proven to be far more challenging.

The journey has involved many disappointments and occasionally a small success.

I define success in very practical terms: a client who genuinely invests in continuous monitoring. A client who not only identifies anomalies but also investigates root causes, implements corrective actions, and is willing to connect those insights to a data-driven audit approach.

When that happens, real value is created.

Many of the larger ambitions I have written about over the years—such as real-time assurance, assurance across supply chains, ecosystem assurance, and customized assurance—remain, for now, interesting visions of the future.

That does not mean they are impossible.

It simply means that practice often moves much slower than technology.

Question 3 – Is There a Safe Place for LLMs in Audit?

My third question brings us to the topic that dominates almost every conference today.

The rise of generative AI.

In a remarkably short period of time, our profession has become fascinated by large language models.

First came terms such as AI-driven auditing and AI-powered auditing.

Then we discovered that, in practice, much of the discussion revolves around using LLMs for technical support, document analysis, script generation, and various forms of productivity enhancement.

My own organization struggles with these questions every day.

We come from a world where auditability, reproducibility, explainability, and confidentiality of information are fundamental principles.

At the same time, we are confronted with entirely new challenges involving shadow AI, audit trails, data security, training, quality assurance, and regulatory oversight.

My third question is therefore:

Does a safe and robust way of applying large language models within auditing already exist, or are we currently creating a new Wild West in which speed and possibilities sometimes seem more important than quality and control?

Question 4 – How Are We Going to Audit AI?

This brings me to the question that personally occupies me perhaps the most.

How are we actually going to audit AI?

I fully understand why there is currently so much attention on AI governance, the AI Act, standards, documentation, and implementation challenges.

These are important topics.

But for me, assurance is ultimately not about how a system is designed.

It is about how a system behaves.

How will we audit dynamic pricing algorithms?

How will we assess real-time decision-making systems?

How do we obtain sufficient audit evidence over systems that continue to learn and evolve?

How do we audit a black box when its outputs directly influence business processes and potentially financial statements?

To me, this is where a fundamental challenge for our profession lies.

Not so much AI Assurance.

But rather: How To Audit AI.

Five Lessons from 31 Years in Practice

Looking back on more than thirty-one years in accounting and my own modest contribution to innovation, I arrive at five lessons.

The first lesson is that the greatest obstacle to innovation in accounting has rarely been technology.

It has almost always been human behavior.

We like to talk about systems, methodologies, standards, and tools, but time and again it turns out that only a relatively small group of professionals is willing to integrate new technology structurally into everyday work.

The second lesson is that it is a misconception that organizations are already fully data-driven.

Many data-driven auditing projects stalled the moment analytics started producing actual findings. Enthusiasm for dashboards, analytics, and insights often appears inversely proportional to the number of exceptions that become visible.

The third lesson is that our profession sometimes suffers from a remarkably high level of FOMO.

Blockchain was going to transform auditing.

Big Data was going to transform auditing.

Machine learning was going to transform auditing.

AI-driven auditing was going to transform auditing.

Human-free auditing was going to transform auditing.

And now agentic AI and autonomous agents are already knocking on the door.

Every new technology creates excitement, but also noise. That noise affects clients, regulators, and young professionals trying to understand what the future of the profession will look like. Sometimes we create expectations that practice simply cannot yet fulfill.

The fourth lesson is that internal monitoring and external auditing remain far less connected than technology would allow.

For almost twenty years, I have believed that enormous opportunities lie there—perhaps even greater opportunities than in many of the technologies currently attracting our attention.

My fifth lesson may be the most important of all.

What I currently miss is a transparent and collective conversation within our assurance ecosystem about where we actually want to go as a profession.

Not only from a technology perspective.

But also from the perspectives of methodology, implementation, education, quality management, and supervision.

The developments around AI and LLMs only make that need more urgent.

At the moment, I see many initiatives, many experiments, and a great deal of enthusiasm.

What I see less of is a shared vision of the journey we want to take together as a profession.

Perhaps that is the most important question of today.

Not which technology comes next.

Not which tool will be introduced next.

But how we, as a profession, will collectively shape the future of assurance.

Because if there is one thing I have learned over the past thirty-one years, it is that technology has rarely been the real problem.

The greatest barrier to innovation in accounting has almost always been human behavior.

I am curious to hear how my fellow panelists view this.